What Are “Bad Credit” Credit Cards?

“Bad credit” credit cards are designed for people with a low credit score or a limited credit history. In the UK, these cards are often used as a starting point for rebuilding financial credibility after missed payments, defaults, or a lack of borrowing history. They typically offer lower credit limits and higher interest rates compared to mainstream cards.

Lenders still carry out checks before approval. Even though these cards are easier to access, they are not guaranteed. Providers must follow rules set by the Financial Conduct Authority, which means they assess affordability and clearly explain the terms before offering credit.

How These Cards Work

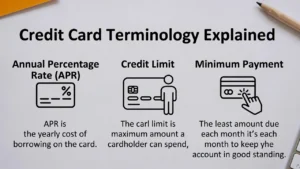

A bad credit card works like any standard credit card. You can use it for purchases, receive a monthly statement, and make repayments. The difference lies in the conditions attached. Credit limits are usually modest, often starting between £200 and £1,000, and interest rates are generally higher.

Your usage is reported to UK credit reference agencies such as Experian, Equifax, and TransUnion. This means your repayment behaviour directly affects your credit profile over time.

Who Might Consider a Bad Credit Card?

These cards may be suitable for individuals who have:

A history of missed or late payments

Defaults or County Court Judgements (CCJs)

Little or no previous credit activity in the UK

They are not intended for long-term borrowing or large purchases. Instead, they act as a tool to demonstrate improved financial behaviour. If you already qualify for a standard credit card with a lower APR, that option may be more cost-effective.

Key Features to Expect

Bad credit cards usually come with stricter limits and fewer rewards. Many do not offer cashback or travel perks. Instead, the focus is on access to credit and reporting repayment activity.

You may also notice higher representative APRs. This reflects the increased risk for lenders. It is important to understand that interest can accumulate quickly if you carry a balance.

Costs and Limitations

| Feature | What It Means | Why It Matters |

|---|---|---|

| Low Credit Limit | Smaller borrowing capacity | Helps reduce risk but limits spending |

| Higher APR | More expensive borrowing | Paying in full avoids interest |

| Limited Rewards | Few or no perks | Focus is on credit building |

| Eligibility Checks | Based on affordability | Not all applicants are approved |

| Credit Reporting | Activity shared with agencies | Builds or harms your credit profile |

This table highlights that these cards are structured for controlled use rather than flexibility or rewards.

How to Use These Cards Responsibly

Using a bad credit card effectively requires discipline. Start with small, manageable purchases such as groceries or monthly subscriptions. Repay the full balance whenever possible to avoid interest charges.

Keeping your credit utilisation low is also important. For example, if your limit is £300, try not to exceed £90 at any time. This shows lenders that you are not overly reliant on credit.

Setting up a direct debit can help ensure that payments are made on time. Even one missed payment can negatively impact your progress.

Risks to Be Aware Of

While these cards offer access to credit, they can become expensive if misused. Carrying a balance over several months may lead to high interest costs. Late payment fees can also apply and may be recorded on your credit file.

Applying for multiple cards within a short period may reduce your chances of approval. Each application can leave a footprint on your credit report, which lenders may view as a sign of financial stress.

Realistic Expectations

Improving your credit score takes time. A bad credit card does not fix your credit instantly. Consistent repayment behaviour over several months or longer is usually required before noticeable improvement appears.

Some providers may review your account after a period of responsible use and offer a higher credit limit or upgrade options. However, this is not guaranteed and depends on your financial behaviour.

Final Thoughts

Low credit score or “bad credit” credit cards can provide a practical route to rebuilding your credit profile in the UK. They offer access where other products may not, but they come with higher costs and stricter conditions.

If used carefully, they can support gradual improvement in your credit history. If used without a clear repayment plan, they may increase financial pressure. Understanding how these cards work before applying is essential for making informed decisions.

Frequently Asked Questions

Can I get a credit card with a low credit score in the UK?

Yes, some lenders offer credit cards specifically for people with low or limited credit history. Approval depends on your financial situation, including income and affordability checks, so it is not guaranteed.

Do bad credit credit cards improve your credit score?

They can help if used responsibly. Making payments on time and keeping balances low is reported to agencies like Experian, Equifax, and TransUnion, which may gradually improve your credit profile.

Why do bad credit cards have higher interest rates?

Higher APR reflects the increased risk to lenders when offering credit to individuals with lower credit scores. This is why paying the full balance each month is usually the most cost-effective approach.

What credit limit can I expect with a bad credit card?

Limits are usually lower than standard cards, often starting from around £200 to £1,000. The exact amount depends on your credit profile and affordability assessment.

Should I apply for multiple bad credit cards at once?

Applying for several cards in a short period may reduce your chances of approval and affect your credit file. It is generally better to check eligibility first and apply selectively.