- Understanding Credit Card Refunds

- How the Refund Process Works

- Returns vs Refunds: What’s the Difference?

- Section 75 Protection in the UK

- Chargeback: Another Refund Option

- What Happens to Interest and Payments?

- Key Differences at a Glance

- Common Situations and Outcomes

- Things to Watch Out For

- Final Thoughts

- Frequently Asked Questions

Understanding Credit Card Refunds

When you return an item purchased with a credit card in the UK, the refund is usually sent back to the same card rather than given as cash. This process is handled by the retailer, but the money flows through your card provider before appearing on your account. Because credit cards involve borrowing rather than direct spending, refunds reduce your outstanding balance instead of increasing your bank balance.

The process is regulated under UK consumer rules overseen by the Financial Conduct Authority, which ensures transparency in how payments, refunds, and disputes are managed.

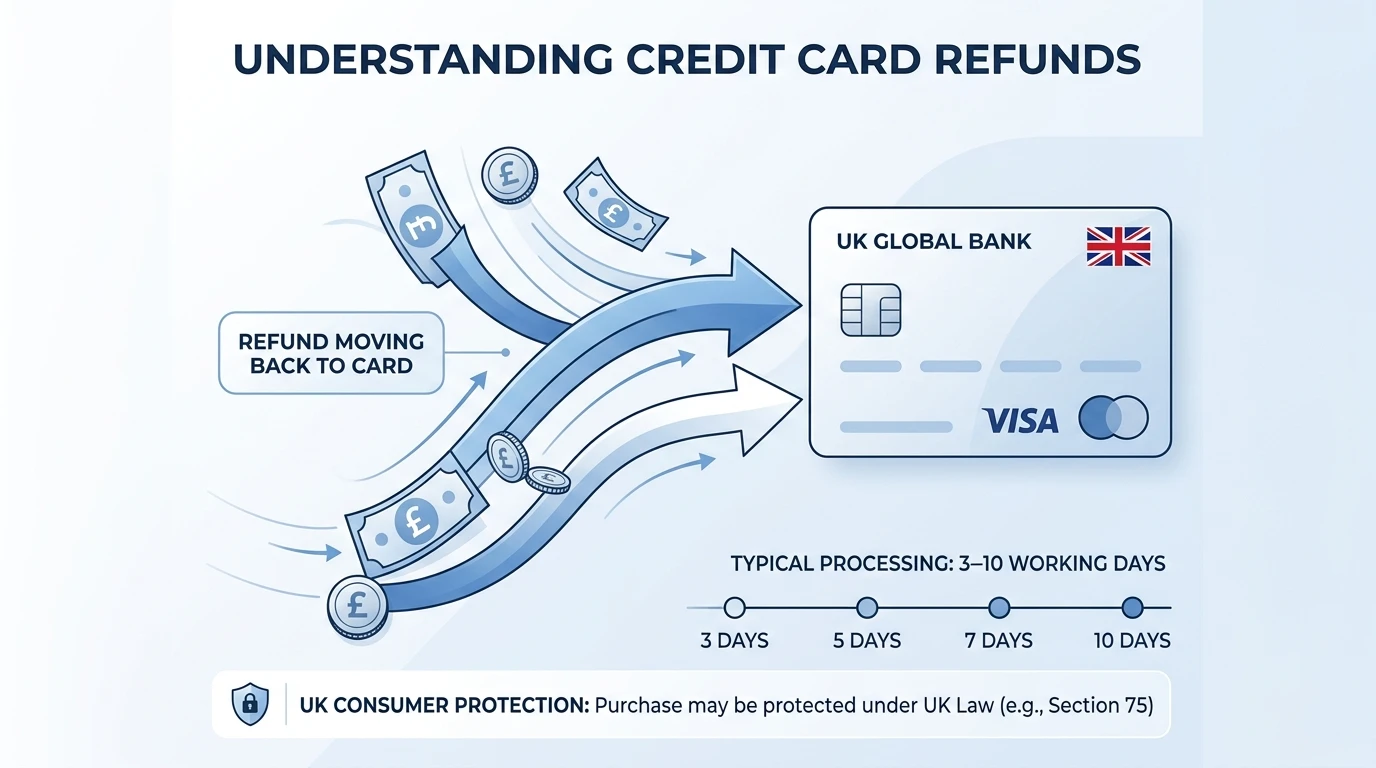

How the Refund Process Works

When a refund is issued, the retailer sends a reversal request through the payment network. Your card provider then processes this and updates your account. This usually takes between 3 and 10 working days, although it can vary depending on the merchant and payment system.

If you have already paid off your balance, the refund may create a positive balance on your card. This can either be used for future purchases or, in some cases, requested as a transfer back to your bank account.

Returns vs Refunds: What’s the Difference?

A return is when you give the product back to the retailer, while a refund is the financial transaction that follows. Not all returns automatically result in a full refund. Some retailers may offer exchanges, store credit, or partial refunds depending on their policy.

It is important to check the retailer’s terms before purchasing, especially for online orders or sale items. Your rights may differ based on whether the item is faulty, unwanted or misdescribed.

Section 75 Protection in the UK

One of the key benefits of using a credit card in the UK is protection under the Consumer Credit Act 1974 Section 75. This applies to purchases between £100 and £30,000. If something goes wrong, such as goods not arriving or being faulty, you may be able to claim a refund directly from your card provider.

This protection makes credit cards different from debit cards. The card provider shares responsibility with the retailer, which can provide an additional layer of security for larger purchases.

Chargeback: Another Refund Option

Chargeback is a separate process from Section 75. It allows you to dispute a transaction through your card provider if there is an issue with the purchase. Unlike Section 75, chargeback is not a legal right but a scheme-based process used by card networks. credit-card-eligibility-checker.

It may apply to smaller purchases under £100 or situations where Section 75 does not cover the transaction. Time limits usually apply, so it is important to act quickly if there is a problem.

What Happens to Interest and Payments?

If you return an item before your statement is generated, the refund may reduce your balance before interest is calculated. However, if the refund is processed after your statement date, you may still need to make at least the minimum payment.

Interest may still apply temporarily until the refund is fully processed. Once applied, the refund should reduce the balance and any related interest over time.

Key Differences at a Glance

| The card provider may refund directly | How It Works | What to Expect |

|---|---|---|

| Standard Refund | Retailer processes return | Money goes back to your card balance |

| Paid Balance Refund | Account already cleared | Creates positive balance or credit |

| Section 75 Claim | Legal protection for £100–£30,000 | Card provider may refund directly |

| Chargeback | Dispute via card network | Used for smaller or disputed transactions |

| Delayed Refund | Processing time varies | The card provider may refund directly |

Common Situations and Outcomes

If you cancel an online order before it is dispatched, the refund is usually processed quickly. For faulty goods, you may be entitled to a full refund depending on consumer rights. In cases where a company goes out of business, Section 75 protection can become particularly valuable.

For partial refunds, such as returned items from a larger order, only the relevant portion of the balance is adjusted. This means you still need to manage any remaining balance as normal.

Things to Watch Out For

Refunds are not always instant, and delays can happen if the retailer takes time to process the return. It is also possible for refunds to appear as “pending” before being fully applied. During this time, your available credit may not update immediately.

If you have a dispute, keeping receipts, emails, and order confirmations can make the process smoother. Clear records help both the retailer and your card provider understand your claim.

Final Thoughts

Credit card refunds in the UK are generally straightforward, but the timing and method can vary depending on the situation. Understanding the difference between returns, refunds, Section 75 protection, and chargeback processes can help you manage your account more effectively. While credit cards offer added protection, staying organised and aware of your statements ensures you avoid confusion or unexpected charges.

Frequently Asked Questions

1. How long does a credit card refund take in the UK?

Most credit card refunds in the UK take between 3 to 10 working days to appear on your account. The exact time depends on the retailer and payment network. Some refunds may show as pending before being fully processed.

2. Do refunds go back to my bank account or credit card?

Refunds are usually sent back to the same credit card used for the purchase. If your balance is already cleared, the refund may create a positive balance that can be used for future spending or transferred to your bank.

3. What is Section 75 protection on credit cards?

Section 75 is a UK legal protection under the Consumer Credit Act 1974 Section 75. It covers purchases between £100 and £30,000 and allows you to claim a refund from your card provider if something goes wrong with the purchase.

⚖️ does not apply to debit cards or American Express (credit provider must be “connected” to retailer)

4. Can I get a refund if a company goes out of business?

Yes, in many cases you can claim through Section 75 if the purchase meets the criteria. You may also use the chargeback process for smaller amounts or where legal protection does not apply.

5. Do I still need to pay my credit card bill if I’m waiting for a refund?

Yes, you should continue making at least the minimum payment. A pending refund does not stop your repayment obligations, and missing payments could result in fees or affect your credit record.

📆 you can request a refund of overpaid interest once the credit appears