Understanding your credit score is one of the most important steps before applying for a credit card in the UK. Lenders use it to decide how risky it is to offer you credit and what limit or interest rate you might qualify for. A good credit score can mean lower interest rates and higher chances of approval, while a lower score may restrict your options.

Even if you have never missed a payment, your score reflects your financial habits, including how much credit you use compared to your limits. Knowing where you stand can help you make smarter choices and avoid unnecessary rejections.

What is a credit score?

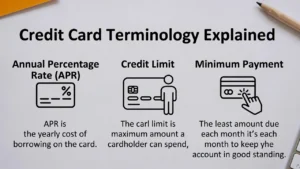

A credit score is a number that summarises your creditworthiness. In the UK, scores from Experian, Equifax, and TransUnion help lenders understand how responsible you are with borrowed money. Scores generally range from poor to excellent, affecting approval chances and card features.

How lenders check your credit

When you apply for a credit card, the provider performs a credit check. A hard search can slightly lower your score temporarily, while a soft searchlike using a loan eligibility checker, does not. Lenders also review your credit history, existing debts, and repayment patterns before making a decision.

Why credit scores matter for approval

Lenders consider your score to set the credit limit and interest rate. A higher score signals reliability, potentially unlocking cards with rewards, cashback, or 0% offers. Lower scores may limit you to credit builder cards or cards with smaller limits and higher APRs.

Improving your credit score before applying

Paying bills on time, keeping balances low, and avoiding multiple applications at once can all help improve your score. Regularly checking your credit report ensures there are no errors that might affect your approval.

Common myths about credit scores

Some believe checking their own score lowers it. This is false if done via a soft search. Others think closing old accounts boosts their score, but it can reduce your credit history length and harm your rating. Understanding these nuances is key to better credit decisions.

Practical UK examples

If your credit score is 750 or above, you may qualify for a rewards card with a £5,000 limit. Scores around 600 might only allow a credit builder card with a £500 limit. These examples show how scores directly influence card options and borrowing power.

Conclusion

Your credit score is a vital factor in UK credit card approval. By understanding how it works, monitoring your score, and using responsible financial habits, you can increase your chances of approval and access better card features without unnecessary fees or rejections.

Frequently Asked Questions

Can a low credit score stop me from getting a card?

Yes, many standard credit cards require a minimum score. However, credit builder cards are designed to help people with lower scores improve their credit history.

UK lenders assess eligibility individually; checking eligibility leaves only a soft footprint.Does checking my credit score affect approval?

Soft searches do not impact your score, but hard searches made by lenders during applications may slightly lower it temporarily.

How often should I check my credit report?

Once every 3–6 months is sufficient to spot errors and track improvements. Frequent checks via a soft search are safe.

Can paying off debts improve my credit score?

Yes, reducing outstanding balances lowers your credit utilisation ratio, which can positively affect your score.

Keeping credit utilisation below 30% is often recommended by UK agencies.Are all UK credit reference agencies the same?

No. Experian, Equifax, and TransUnion each use slightly different scoring models, so your score may vary slightly across agencies.