- Understanding Cash Flow in Everyday Finances

- Using Credit Cards to Track Spending

- Interest-Free Periods and Budget Planning

- Example of Budgeting with a Credit Card

- Benefits and Potential Risks

- Maintaining Responsible Credit Use

- When Credit Cards May Not Help Budgeting

- Conclusion

- Frequently Asked Questions About Credit Unions

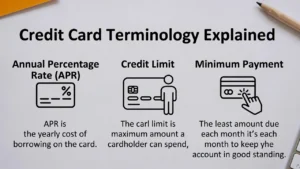

Credit cards are often viewed mainly as borrowing tools, but they can also support better budgeting and short-term cash flow management when used responsibly. In the UK, many people use credit cards to organise spending, track expenses, and manage payments between income dates. The key advantage is that credit cards provide an interest-free period on purchases if the full balance is paid on time.

Understanding how this system works can help individuals plan their finances more effectively. UK credit cards operate under consumer protection rules set by the Financial Conduct Authority, which require lenders to clearly explain fees, interest rates, and repayment obligations. This transparency helps cardholders understand how their spending fits within a wider financial plan.

Understanding Cash Flow in Everyday Finances

Cash flow refers to the timing of money coming in and going out. For example, many people receive income once a month but face regular expenses throughout that period. A credit card can act as a short-term bridge, allowing purchases to be made while keeping bank account balances stable until the next salary arrives.

This approach only works if spending is controlled and the balance is cleared before interest applies. When used this way, a credit card functions as a payment management tool rather than a long-term debt source.

Using Credit Cards to Track Spending

One practical advantage of credit cards is the detailed statement provided each month. These statements categorise transactions such as groceries, travel, or entertainment. Reviewing this information can help identify spending patterns and areas where adjustments may be needed.

Digital banking apps often provide additional features such as alerts, spending summaries, and budgeting tools. These insights can make it easier to monitor monthly spending without manually tracking every purchase.

Interest-Free Periods and Budget Planning

Most UK credit cards offer an interest-free period on purchases, typically between 40 and 56 days. This means you can make purchases during the billing cycle and avoid interest if the full balance is repaid by the due date.

For budgeting purposes, this creates a predictable timeline:

You spend using the credit card during the month

A statement summarises the total balance owed

You repay the full amount before the payment deadline

This cycle can help align spending with income, making it easier to manage monthly budgets.

Example of Budgeting with a Credit Card

Imagine someone earns £2,000 per month and spends around £800 on groceries, transport and bills. Instead of paying each expense immediately from their bank account, they use a credit card for these purchases. credit card eligibility checker.

At the end of the billing cycle, they receive a statement for £800. If they pay the full amount from their salary before the due date, no interest is charged. This method allows them to maintain cash in their bank account until repayment time, improving short-term financial flexibility.

Benefits and Potential Risks

Credit cards can support budgeting, but only if spending remains controlled. Carrying a balance from month to month can lead to interest charges that undermine financial planning.

The table below summarises common benefits and potential risks.

| High balances may affect the credit profile | Potential Benefit | Possible Risk |

|---|---|---|

| Expense Tracking | Monthly statements show spending categories | Ignoring statements can hide overspending |

| Interest-Free Period | Short-term flexibility for purchases | Interest applies if balance not repaid |

| Payment Timing | Align spending with salary dates | Missing payments can lead to fees |

| Credit Record | Responsible use may support credit history | High balances may affect credit profile |

Understanding these factors helps ensure the card supports budgeting rather than creating financial pressure.

Maintaining Responsible Credit Use

Using a credit card for budgeting requires discipline. Setting a monthly spending limit based on your income can prevent unexpected debt. Many people also set up direct debits for the full balance each month to avoid missing payments.

Monitoring your credit utilisation is also important. This refers to the proportion of your credit limit that is currently used. Keeping this ratio relatively low may reflect positively on your credit profile over time.

When Credit Cards May Not Help Budgeting

A credit card may not be the best budgeting tool if spending habits are difficult to control or if minimum payments are the only affordable option. In those situations, the cost of interest can quickly increase financial pressure.

Alternative budgeting strategies, such as prepaid cards or debit-based spending plans, may provide clearer spending limits. The most suitable method depends on individual financial circumstances and spending behaviour.

Conclusion

Credit cards can support budgeting and cash flow management when used thoughtfully. Features such as monthly statements, interest-free periods, and digital spending tools allow cardholders to monitor expenses and align repayments with income. However, these benefits depend on disciplined spending and timely repayment. By treating a credit card as a structured payment tool rather than a borrowing solution, it can become a useful part of everyday financial planning in the UK.

Frequently Asked Questions About Credit Unions

Yes, credit cards can support budgeting by providing detailed monthly statements and transaction records. These records make it easier to track where money is being spent and compare spending against a planned monthly budget.

Most UK credit cards offer an interest-free period on purchases, typically between 40 and 56 days. If the full balance is repaid before the due date, interest is usually not charged on those purchases.

Responsible use may influence your credit profile over time. Making payments on time and keeping balances within the limit can show lenders that you manage credit responsibly. Credit activity is reported to agencies such as Experian and Equifax.

Paying the full statement balance each month generally avoids interest charges and helps keep borrowing costs low. It also prevents balances from building up over time.

Credit cards can help manage unexpected or irregular expenses by allowing short-term flexibility in payment timing. However, this approach works best when the balance can be repaid before interest applies.