Applying for a credit card in the UK is more than just filling out a form. Providers look at your financial habits, income, and credit history to ensure you can manage repayments responsibly. Understanding what lenders consider can save time, improve your chances of approval, and help you choose a card that suits your lifestyle.

Applying for a credit card in the UK requires meeting certain basic conditions. Most providers expect you to be at least 18 years old and have a permanent UK address. Lenders also want evidence of a stable income, whether from employment, self-employment, or certain benefits. These factors help them assess whether you can responsibly manage repayments. Even if you meet the age and residence requirements, your financial history plays a big role in whether your application is accepted.

Understanding Credit Checks

When you apply, lenders will carry out a credit check to evaluate your borrowing risk. In the UK, this can be a hard search, which may slightly impact your credit score, or a soft search, which does not affect it. Hard searches are common when formally applying for a card, while soft searches are often used by eligibility checkers or pre-approval tools to see which cards you might qualify for. Understanding the difference helps you manage your credit record while exploring options.

The Role of Your Credit History

Your past credit behaviour is a major factor in determining eligibility. Lenders review your credit report for missed payments, outstanding debts, defaults, or County Court Judgments (CCJs). A consistent record of timely payments increases your chances of approval, whereas multiple missed payments or high credit utilisation can reduce the likelihood. Even new applicants with limited credit history may be offered entry-level cards designed to help build a positive credit record over time.

Income and Employment Requirements

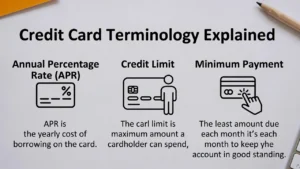

Most UK credit card providers require proof of income to ensure you can meet monthly repayments. This does not mean you must be salaried; self-employed individuals or those receiving regular benefits may also qualify. Lenders use income to determine your credit limit, balancing the risk of lending with your repayment capacity. A clear and stable income record helps build trust with the provider and can lead to better credit offers.

Additional Considerations

Other factors can affect eligibility, such as existing credit commitments, outstanding loans, or multiple simultaneous applications. Lenders may also consider your residency status and how long you’ve lived at your current address. While eligibility criteria differ slightly between banks, all UK providers operate under the oversight of the Financial Conduct Authority (FCA), ensuring fair treatment and transparency for applicants.

How to Check Your Eligibility Safely

Before applying, using a loan eligibility checker offered by most UK card providers is a safe way to gauge approval chances. These tools perform a soft search on your credit file, providing guidance without impacting your score. They can suggest the types of cards you are likely to be accepted for, helping you make informed choices and reducing the risk of multiple unsuccessful applications.

Building Eligibility Over Time

If you don’t immediately meet the criteria for mainstream credit cards, you can build your eligibility gradually. Starting with a credit builder card, paying all bills on time, and keeping credit utilisation low helps strengthen your credit history. Over time, this improves your chances of qualifying for higher-limit cards, rewards cards, or cards with better interest rates, giving you more flexibility in managing your finances.

Key Takeaway

Eligibility for UK credit cards is about more than age or income; it involves your credit history, repayment behaviour, and financial stability. By understanding the criteria, checking your options safely, and managing your credit responsibly, you can improve your chances of being approved for a card that suits your lifestyle and financial goals.

Frequently asked questions – credit cards (UK)

1. Who can apply for a credit card in the UK?

Anyone aged 18 or over with a permanent UK address can apply. Lenders also consider income, employment status, and financial commitments to determine your eligibility and credit limit.

2. What is the difference between a hard and soft credit check?

A hard credit check is recorded on your credit file and may slightly affect your score, while a soft check is invisible to lenders and used for eligibility checkers. Soft checks help you see likely approval without impacting your credit rating.

3. Can I get a credit card with no credit history?

Yes, beginners can apply for credit builder cards. These help establish a credit record by showing lenders you can manage repayments responsibly, improving eligibility for standard cards in the future.

4. How does my income affect credit card approval?

Lenders use your income to assess repayment ability and decide your credit limit. Higher or stable income increases the likelihood of approval, while low or inconsistent earnings may limit your options or the maximum credit available.

5. What happens if my application is refused?

If refused, the provider must tell you why and which credit reference agency they used. You can review your credit file, address any errors, and reapply in the future once your credit profile improves.