- What Is a Credit Card? (UK Overview)

- Key UK Credit Card Terms Explained

- Credit Checks in the UK Explained

- Types of Credit Cards in the UK

- Credit Card Fees and Charges Breakdown

- Practical UK Examples

- Comparison Table: Key Credit Card Terms at a Glance

- Common Credit Card Mistakes UK Borrowers Make

- How to Choose the Right Credit Card in the UK

- The Bottom Line: Understanding Credit Card Terms Before You Apply

- Frequently Asked Questions (credit cards – UK edition)

Understanding credit card terminology is essential before applying for a credit card in the United Kingdom. Terms like APR, credit limit, minimum payment, and balance transfer frequently appear in adverts and statements, but they are not always clearly explained.

Credit cards are regulated financial products in the UK, overseen by the Financial Conduct Authority (FCA). Consumer protections such as Section 75 of the Consumer Credit Act 1974 also provide legal safeguards for certain purchases.

This guide explains key UK credit card terms in plain language, includes practical examples in GBP, and outlines how credit checks and fees work, helping you make informed decisions.

What Is a Credit Card? (UK Overview)

A credit card is a form of revolving credit. This means you can borrow up to a set limit, repay some or all of it, and borrow again.

Unlike a debit card, which uses money from your current account, a credit card allows you to borrow funds from a lender and repay later.

Who Regulates Credit Cards in the UK?

Credit card providers must follow rules set by the Financial Conduct Authority. These rules require lenders to:

- Show a representative APR

- Assess affordability

- Provide clear fee disclosures

- Offer support for customers in financial difficulty

Certain purchases between £100 and £30,000 may also be protected under Section 75, meaning the lender can share responsibility if goods are faulty or not delivered.

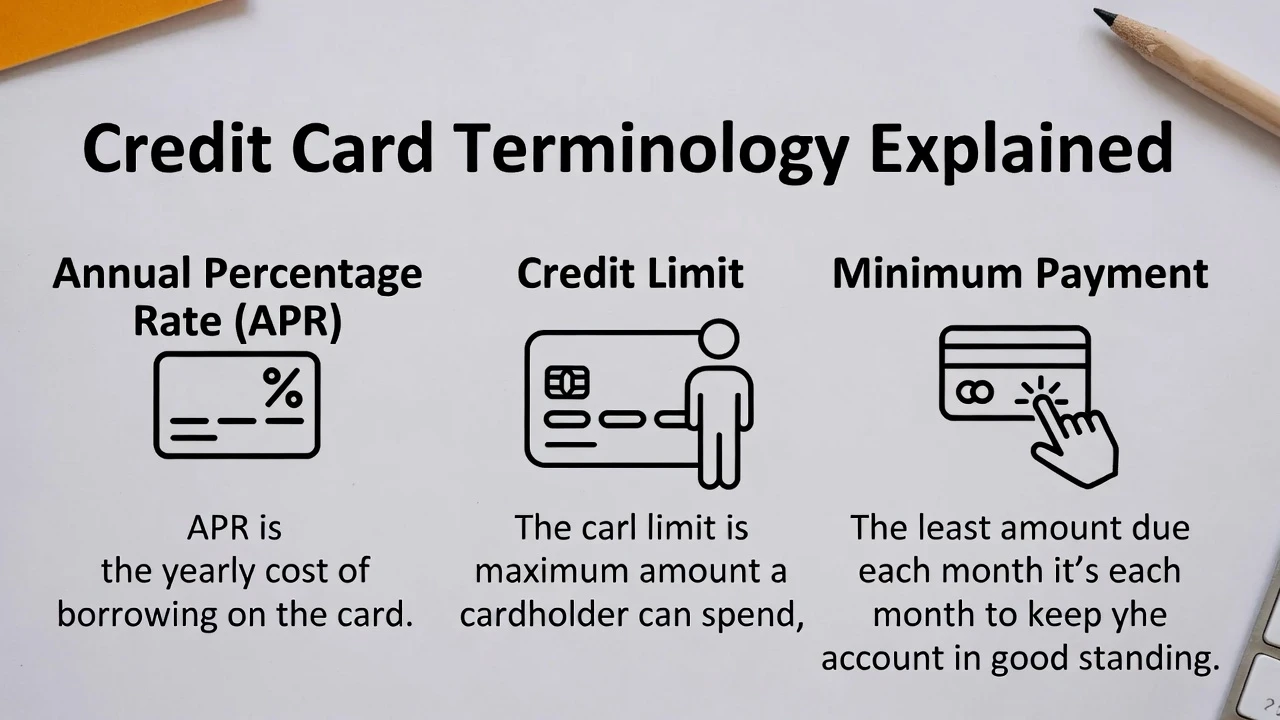

Key UK Credit Card Terms Explained

APR (Annual Percentage Rate)

APR represents the yearly cost of borrowing, including interest and standard charges.

Types of APR include:

- Representative APR – The rate at least 51% of approved customers receive.

- Variable APR – Can change based on market conditions.

- Fixed APR – Stays the same for a set period.

- Purchase APR – Applies to spending.

- Cash Advance APR – Usually higher and applied immediately.

In the UK, most cards advertise a representative variable APR.

Credit Limit

Your credit limit is the maximum amount you can borrow.

Lenders decide this based on:

- Income

- Credit history

- Existing debts

- Affordability checks

For example, if your limit is £3,000 and you spend £1,500, your credit utilisation is 50%. High utilisation can affect your credit score.

Going over your limit may result in fees and potential credit file impact.

Minimum Payment

The minimum payment is the smallest amount you must pay each month.

It is usually calculated as:

- A percentage of your balance (e.g. 2–3%)

OR - A fixed minimum (e.g. £5)

If you owe £2,000 and the minimum is 2%, you may need to pay £40.

Paying only the minimum increases the total interest paid and extends repayment time.

Setting up a Direct Debit can help avoid missed payments.

Billing Cycle & Interest-Free Period

A billing cycle typically lasts around one month. If you repay your full balance by the due date, you may benefit from an interest-free period (usually up to 56 days on purchases).

Interest-free periods do not apply to cash withdrawals.

Chargeback vs Section 75 Protection

Section 75 applies to purchases between £100 and £30,000 and makes the lender jointly liable with the retailer.

Chargeback is a voluntary scheme (not law) allowing cardholders to dispute transactions under certain circumstances.

Credit Checks in the UK Explained

Hard Search vs Soft Search

- Soft search: Does not affect your credit score (used for eligibility checks).

- Hard search: Recorded on your file and may impact your score temporarily.

Multiple hard searches in a short period can signal higher risk to lenders.

UK Credit Reference Agencies

Lenders use information from:

- Experian

- Equifax

- TransUnion

Each agency may calculate scores differently.

Types of Credit Cards in the UK

Different types serve different purposes:

- Balance transfer cards

- 0% purchase cards

- Credit builder cards

- Rewards & cashback cards

- Travel cards

- Student cards

- Secured cards

- Business credit cards

- Prepaid cards (not true credit cards)

Credit Card Fees and Charges Breakdown

Common UK fees include:

- Balance transfer fee (2–5%)

- Late payment fee

- Cash withdrawal fee

- Foreign transaction fee (often around 3%)

- Annual fee (on some premium cards)

Understanding total cost is more important than focusing only on promotional rates.

Practical UK Examples

Example 1 – Paying Only the Minimum

If you owe £2,000 at 24% APR and only pay the minimum, repayment could take several years and cost hundreds in interest.

Example 2 – 0% Balance Transfer

Transferring £3,000 with a 3% fee costs £90 upfront. If cleared before the 0% period ends, interest savings may outweigh the fee.

Example 3 – Section 75 Claim

If you buy furniture costing £800 and the retailer collapses, you may claim through your credit card provider.

Example 4 – Hard Search Impact

Applying for four cards in one month may temporarily lower your credit score.

Comparison Table: Key Credit Card Terms at a Glance

| Term | What It Means | Why It Matters | UK Risk Factor |

|---|---|---|---|

| APR | Annual borrowing cost | Determines interest paid | Higher APR increases total cost |

| Credit Limit | Maximum borrowing amount | Affects utilisation ratio | Going over may harm credit file |

| Minimum Payment | Smallest monthly repayment | Keeps account active | Long-term interest costs |

| Balance Transfer | Moving debt to new card | Can reduce interest | Fees + promo expiry |

| Section 75 | Legal purchase protection | Consumer safeguard | Only applies £100–£30,000 |

| Hard Search | Full credit check | Affects approval chances | Too many reduce score |

Common Credit Card Mistakes UK Borrowers Make

- Paying only the minimum consistently

- Missing promotional deadlines

- Applying for multiple cards quickly

- Withdrawing cash without understanding fees

- Ignoring foreign transaction charges

How to Choose the Right Credit Card in the UK

Consider:

- Your credit score

- Repayment ability

- Whether you will clear the balance monthly

- Promotional period length

- Total cost including fees

A credit card may suit short-term borrowing or purchase protection needs. For structured long-term borrowing, alternatives such as personal loans may be more predictable.

The Bottom Line: Understanding Credit Card Terms Before You Apply

Credit card terminology can appear complex, but understanding APR, credit limits, minimum payments, and UK protections helps you assess costs and risks clearly.

Before applying, review the total borrowing cost, promotional conditions, and how repayments fit your financial situation.

Frequently Asked Questions (credit cards – UK edition)

What APR is considered good in the UK?

Lower APRs reduce borrowing cost. Many mainstream cards advertise representative APRs above 20%, but the rate you’re actually offered depends on your credit profile and the lender’s assessment. A ‘good’ APR is typically below 12% if you have an excellent credit history; for building cards it can be higher.

Does checking eligibility affect my credit score?

Eligibility checkers (often called ‘soft search’ tools) do not affect your credit file. They give an indication of approval odds without leaving a mark. Only when you formally apply (a ‘hard search’) does it appear on your credit report and may influence your score temporarily.

What happens if I miss a payment?

If you miss a payment you may be charged a late fee (typically £12-15), you could lose any promotional 0% interest deals, and a missed payment marker may be added to your credit file. This can make future credit harder to obtain. Contact your lender immediately if you anticipate difficulty.

Can I get a credit card with bad credit?

Yes — some lenders specialise in credit builder cards or secured cards designed for people with thin or poor credit files. These typically come with lower credit limits (e.g., £200–£1,000) and higher APRs (often around 30–40% APR). Used responsibly, they can help improve your credit score.

Are prepaid cards the same as credit cards?

No, they are fundamentally different. Prepaid cards (e.g., Pockit, Suits Me) let you spend money you load in advance – there’s no borrowing, so they don’t build a credit history. Credit cards extend a line of credit (you borrow and repay later) and can improve your credit file if managed well.