- Introduction

- What Is Dynamic Currency Conversion (DCC)

- Paying in GBP vs Local Currency Abroad

- How Dynamic Currency Conversion Works (Real Example)

- Why You Should Avoid Dynamic Currency Conversion Fees

- Does Paying in Local Currency Save Money

- Foreign Transaction Fees on UK Credit Cards Explained

- Best Credit Cards for Spending Abroad in the UK 2026

- Common Mistakes When Paying Abroad

- Tips to Avoid Currency Conversion Fees When Traveling

- Dynamic Currency Conversion vs Local Currency Quick Comparison

- Final Verdict

- 💱 Frequently asked questionsCurrency & payment abroad

Introduction

When travelling internationally, UK cardholders are often asked whether they want to pay in pounds or the local currency. This choice directly relates to dynamic currency conversion vs paying in GBP, a decision that can significantly impact how much you spend abroad.

Many travellers unknowingly choose the wrong option at payment terminals, leading to hidden costs and higher charges. Understanding whether to pay in GBP or local currency abroad is essential for avoiding unnecessary fees and getting the best exchange rates.

In this guide, you will learn how dynamic currency conversion works, why it is often more expensive, and the smartest way to pay when using UK credit or debit cards overseas.

What Is Dynamic Currency Conversion (DCC)

What is dynamic currency conversion is one of the most common questions among UK travellers. Dynamic Currency Conversion, often called DCC, is a service offered by merchants and ATMs that allows you to pay in your home currency instead of the local currency.

When using dynamic currency conversion UK, the payment terminal converts the transaction into GBP at the point of sale. While this may seem convenient, it usually includes a hidden markup in the exchange rate.

Understanding DCC fees explained UK is important because the rate used is often worse than the rate your bank or card provider would offer.

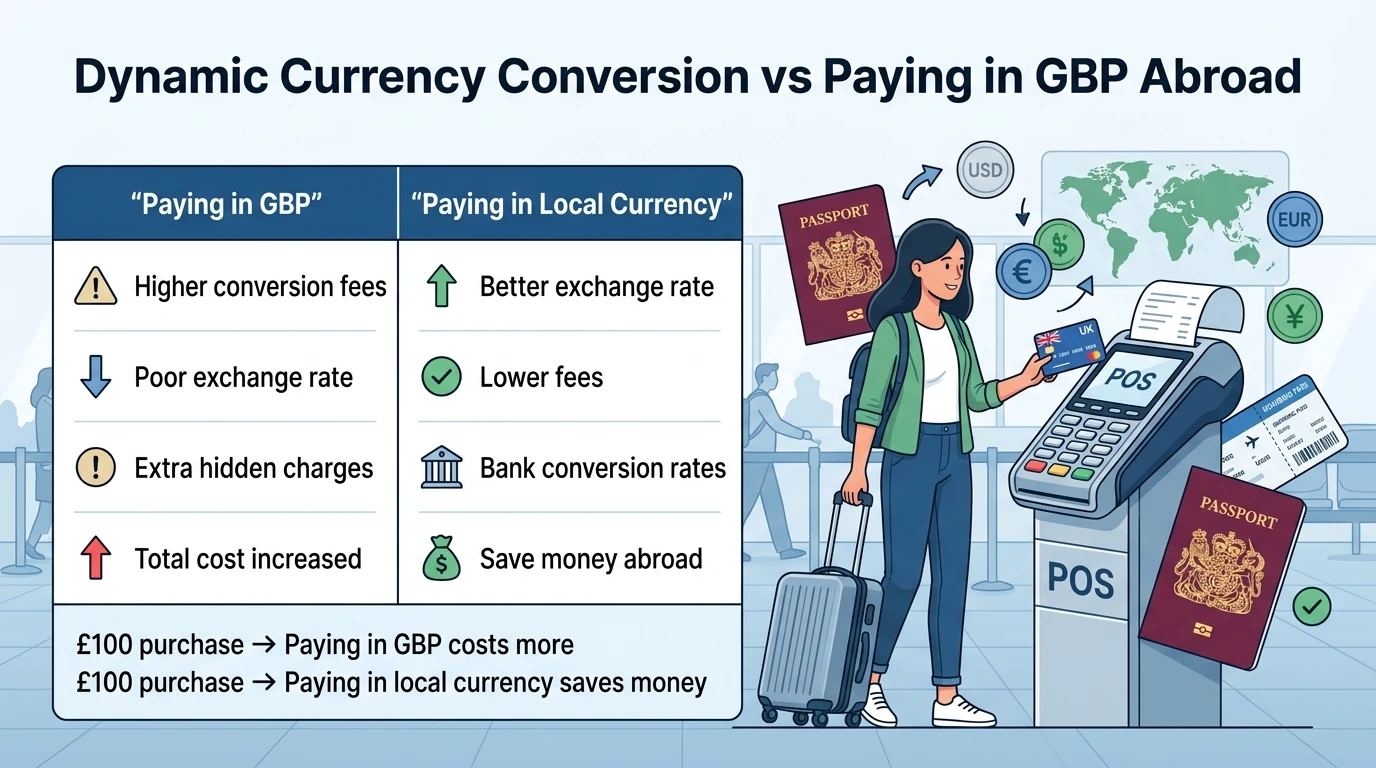

Paying in GBP vs Local Currency Abroad

The choice between pay in local currency vs GBP can determine how much you actually pay for goods and services.

When you choose to should I pay in GBP abroad, the merchant handles the conversion, often adding a markup. On the other hand, paying in local currency allows your bank or card network to process the transaction at a more competitive rate.

In comparisons like paying in GBP vs euros abroad which is better, paying in euros is usually cheaper because it avoids merchant-added conversion fees.

How Dynamic Currency Conversion Works (Real Example)

To understand dynamic currency conversion example UK, consider this scenario.

You spend 100 euros in a European country. If you choose DCC, the terminal converts it into GBP using its own exchange rate, possibly adding 3 to 5 percent markup.

This markup is known as an exchange rate markup and is one of the key components of currency conversion charges UK travellers often overlook.

If you instead pay in euros, your UK card provider converts the amount using interbank rates or network rates, which are typically more favourable.

Why You Should Avoid Dynamic Currency Conversion Fees

There are several reasons to avoid dynamic currency conversion fees UK when travelling.

First, is dynamic currency conversion expensive. In most cases, yes. The conversion rates applied by merchants are rarely competitive.

Second, many travellers ask is dynamic currency conversion a scam UK. While not illegal, it is often misleading because the true cost is not always clearly displayed.

By choosing local currency, you avoid unnecessary markups and ensure better transparency in pricing.

Does Paying in Local Currency Save Money

A common question is does paying in local currency save money. The answer is generally yes.

The best way to pay abroad UK credit cards users should follow is selecting local currency whenever possible. This allows your bank to handle the conversion at a lower cost.

For those looking for the cheapest way to spend money abroad UK, avoiding DCC and using a low-fee card is the most effective strategy.

Foreign Transaction Fees on UK Credit Cards Explained

Even when avoiding DCC, you may still encounter foreign transaction fees that UK credit cards charge. These fees are typically around 2 to 3 percent of each transaction.

Understanding the FX fees UK banks apply is important because they can add up over multiple purchases.

Some overseas card payment charges also include ATM withdrawal fees or additional currency conversion costs, depending on the provider.

Best Credit Cards for Spending Abroad in the UK 2026

Choosing the right card can help minimise costs. The best credit cards for spending abroad in the UK often come with low or zero foreign transaction fees.

Many credit cards with no foreign transaction fees in the UK allow you to spend abroad without additional charges, making them ideal for frequent travellers.

Top UK cards with 0% FX fees are designed specifically for international use, offering better exchange rates and cost savings.

For regular travellers, travel credit cards UK 2026 options also include added benefits such as rewards, insurance, and travel perks.

Common Mistakes When Paying Abroad

Travellers often make costly errors when using cards overseas. One common mistake is selecting GBP instead of the local currency, which leads to higher charges.

Another issue is ignoring the exchange rate markup, which can significantly increase the total cost of transactions.

Understanding these mistakes can help you avoid unnecessary expenses and make smarter payment decisions.

Tips to Avoid Currency Conversion Fees When Traveling

There are several practical ways to avoid currency conversion fees when traveling.

Always choose local currency when given the option at payment terminals or ATMs. This simple step can save money on every transaction.

Using cards with low or zero foreign transaction fees is another effective strategy. Monitoring your transactions and understanding your card’s fee structure also helps reduce costs.

By following these steps, travellers can ensure they are getting the best value when spending abroad.

Dynamic Currency Conversion vs Local Currency Quick Comparison

When comparing DCC with local currency payments, the difference is clear.

DCC offers convenience but includes higher fees and less transparency. Paying in local currency provides better exchange rates and lower overall costs.

For most travellers, local currency is the smarter choice in nearly all situations.

Final Verdict

Understanding dynamic currency conversion vs paying in GBP is essential for UK travellers who want to avoid unnecessary expenses. While DCC may seem convenient, it often leads to higher costs due to hidden markups and unfavourable exchange rates.

The best approach is simple. Always pay in GBP or local currency abroad by choosing local currency whenever possible. Combine this with a low-fee credit card to maximise savings and ensure a smooth travel experience.

By making informed choices, travellers can reduce costs, improve transparency, and make smarter financial decisions when spending abroad.

💱 Frequently asked questions

Currency & payment abroad

You should usually choose the local currency when paying abroad. This helps you avoid hidden fees and ensures you get a better exchange rate from your bank or card provider. When you pick the local currency, your home bank handles the conversion at competitive rates, often near the mid-market rate.

If you choose GBP, the merchant or payment terminal will convert the amount using their own exchange rate. This rate often includes a markup (typically 3–8% higher than the real rate), making the transaction more expensive. In addition, you might incur extra service fees from the local merchant’s bank, which means you end up paying more than necessary.

Yes, dynamic currency conversion (DCC) is usually more expensive because it includes higher exchange rate markups compared to the rates offered by banks or card networks. DCC rates add margins that can make your purchase cost 4% to 10% extra. Banks typically offer rates close to wholesale market levels, while DCC is designed for convenience but hides substantial charges.

You should avoid paying in GBP abroad because it often leads to higher costs due to poor exchange rates and additional hidden fees. Merchants and third-party processors set their own unfavorable rates, and this can turn a simple purchase into an unnecessarily expensive transaction. By paying in the local currency, you allow your card issuer to handle the exchange, which is almost always cheaper and more transparent.

Yes, paying in local currency typically saves money because your bank applies a more competitive exchange rate with lower overall fees. Banks and card networks (Visa/Mastercard) use rates that are close to the mid-market rate with a small transparent fee, whereas DCC markups are much larger. Over multiple transactions, choosing local currency can save you anywhere from 3% to 8% or more on each purchase.