- Understanding the balance transfer concept

- Choosing the right balance transfer card

- Planning a repayment strategy

- Common balance transfer strategies

- Comparing strategy outcomes

- Avoiding common mistakes

- When a balance transfer strategy may not help

- Final thoughts

- Frequently asked questions – balance transfer cards

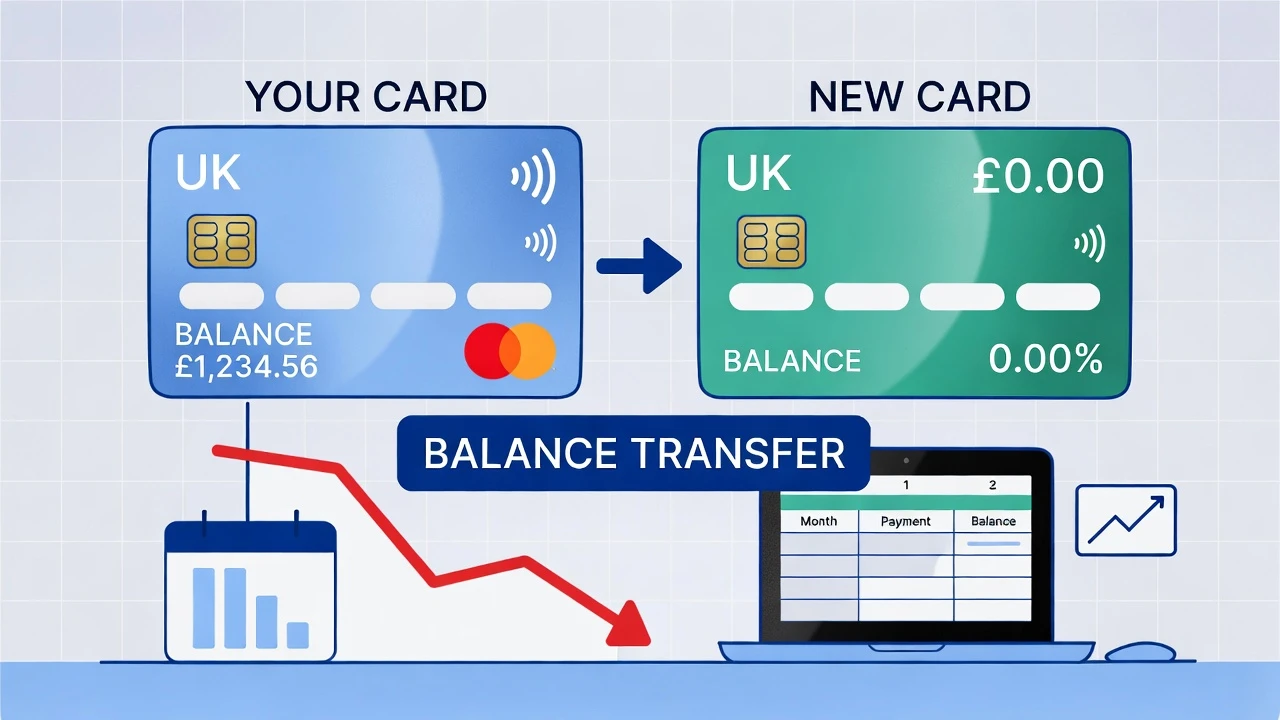

Balance transfer strategies are often used in the UK to reduce the amount of interest paid on existing credit card debt. Instead of continuing to pay a high interest rate on an older card, a borrower moves the balance to another credit card offering a lower or temporary 0% interest rate. This approach can create a structured repayment window where more of each payment goes toward the original balance rather than interest charges.

However, balance transfers are not automatically beneficial in every situation. To actually save money, the transfer must be planned carefully. Factors such as transfer fees, promotional periods, and repayment discipline all affect whether the strategy works effectively.

Understanding the balance transfer concept

A balance transfer means moving outstanding debt from one credit card to another. In many cases, the receiving card offers a promotional interest rate for a limited time. During this period, interest charges are reduced or eliminated, allowing borrowers to focus on repaying the balance itself.

In the United Kingdom, credit card providers must disclose promotional terms clearly under regulations set by the Financial Conduct Authority. These rules ensure consumers can see key details such as the introductory interest rate, the length of the offer, and the standard rate that applies afterward.

Choosing the right balance transfer card

Selecting the right card involves more than simply choosing the longest 0% offer. Borrowers should also consider the transfer fee and the standard interest rate once the promotional period ends.

A longer interest-free period may provide more time to repay the balance, but if the transfer fee is high, the total cost could increase. Some lenders charge a percentage of the transferred balance as a fee, which is added to the new balance.

It is also useful to review eligibility requirements before applying. Lenders typically assess credit history using information from agencies such as Experian, Equifax, and TransUnion.

Planning a repayment strategy

A balance transfer strategy works best when borrowers plan their repayments before moving the debt. The goal should usually be to clear the balance within the promotional period.

For example, if £3,000 is transferred to a card with a 15-month 0% period, dividing the balance by the number of months can help determine a realistic monthly repayment target. Paying around £200 per month in this scenario could clear the balance before interest begins to apply. credit-card-eligibility-checker.

Without a clear repayment plan, borrowers may still face a significant balance when the promotional rate ends.

Common balance transfer strategies

Several approaches can help borrowers manage transferred balances more effectively. One method is the fixed repayment strategy, where the balance is divided evenly across the promotional period.

Another approach is the accelerated repayment method, where borrowers pay more than the minimum payment each month. This reduces the balance faster and lowers the risk of interest charges later.

Some borrowers also combine multiple debts onto one card to simplify payments. While consolidation can make budgeting easier, it should be accompanied by responsible spending habits to prevent the balance from growing again.

Comparing strategy outcomes

| Strategy | How It Works | Potential Benefit | Possible Risk |

|---|---|---|---|

| Fixed repayment plan | Divide balance by promo months | Predictable payments | Requires discipline |

| Accelerated repayment | Pay more than required minimum | Faster debt reduction | May strain monthly budget |

| Debt consolidation | Combine several balances into one card | Simplifies repayment tracking | Risk of new spending |

| Partial transfer | Move only highest-interest debt | Reduces immediate interest cost | Reduces the immediate interest cost |

This comparison highlights that the most effective strategy depends on financial circumstances and repayment capacity.

Avoiding common mistakes

A frequent mistake is continuing to use the old credit card after transferring the balance. If new spending accumulates on the original card, overall debt may increase rather than decrease.

Another common issue is making only the minimum payment on the new card. Minimum payments mainly cover interest and small portions of the balance, which may leave most of the debt unpaid when the promotional period ends.

It is also important to keep track of the promotional expiry date. If a balance remains when the offer ends, the standard APR may apply to the remaining amount.

When a balance transfer strategy may not help

Balance transfer strategies may not be suitable for everyone. If a borrower is already struggling to meet minimum payments, transferring debt without addressing the underlying financial pressure may only delay the problem.

In such situations, independent financial guidance or budgeting adjustments may be more appropriate. Credit solutions should ideally be used as part of a broader financial plan rather than as a short-term fix.

Final thoughts

Balance transfer strategies can reduce interest costs when used responsibly. By selecting the right card, planning repayments carefully, and avoiding unnecessary spending, borrowers may be able to pay off debt more efficiently.

The key principle is preparation. Understanding fees, promotional terms and repayment requirements ensures that a balance transfer works as a practical debt management tool rather than creating additional financial pressure.

Frequently asked questions – balance transfer cards

1. What is a balance transfer credit card in the UK?

A balance transfer credit card allows you to move existing credit card debt from one provider to another, often with a lower or temporary 0% interest rate. This can help reduce interest charges and make it easier to repay the balance over time.

2. Do balance transfers affect your credit score?

Applying for a balance transfer card may trigger a credit check, which can temporarily affect your credit score. However, responsibly managing the transferred balance and making payments on time can support a stronger credit profile in the long term.

3. Is there usually a fee for transferring a balance?

Many UK credit cards charge a balance transfer fee, often a percentage of the amount transferred. For example, a 3% fee on a £2,000 transfer would add £60 to the new balance.

4. Can you transfer balances between cards from the same provider?

Most lenders do not allow balance transfers between cards issued by the same bank or provider. Transfers usually need to be made between different financial institutions.

5. What happens if the balance is not repaid before the promotional period ends?

If a balance remains after the promotional offer expires, the remaining amount will usually start accruing interest at the card’s standard APR. This is why planning repayments during the interest-free period is important.